Hot Dip Tinning Market Forecast 2030: Industry to Reach 1.2 Billion from 812.4 Million in 2026

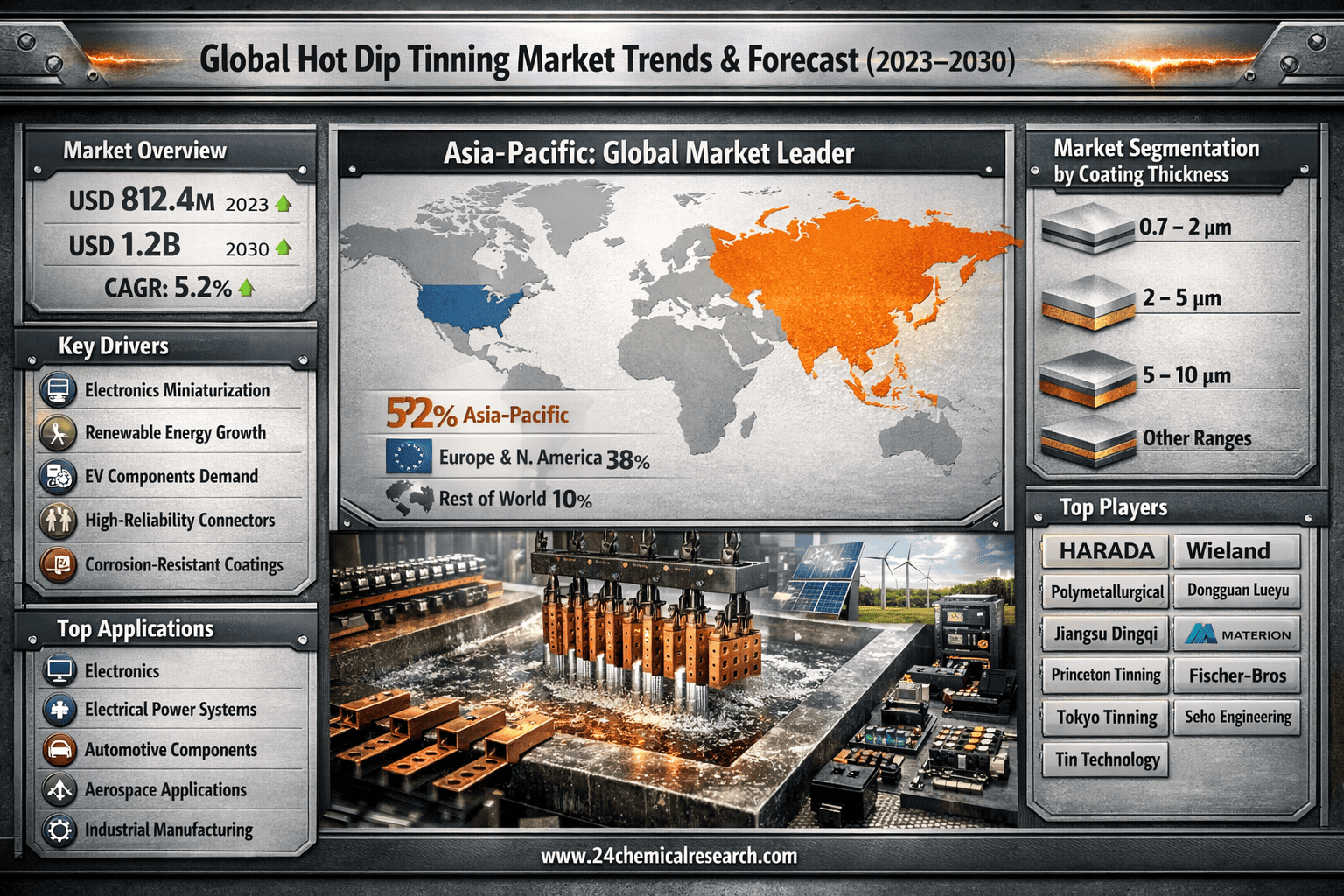

According to 24Chemical Research, Global Hot Dip Tinning market was valued at US$ 812.4 million in 2023 and is projected to reach USD 1.2 billion by 2030, at a CAGR of 5.2% during the forecast period.

Hot Dip Tinning, a long-established metallurgical finishing process, involves immersing metal components—predominantly copper and its alloys—into a bath of molten tin to create a uniform, corrosion-resistant coating. This technology has evolved from traditional industrial applications to become an essential process in modern electronics, electrical engineering, and automotive manufacturing. The resulting tin coating provides exceptional solderability, electrical conductivity, and protection against oxidation, making it indispensable for components requiring reliable connections and long-term durability in demanding environments.

Get Full Report Here: https://www.24chemicalresearch.com/reports/262009/global-hot-dip-tinning-forecast-market-2024-2030-30

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

-

Electronics Miniaturization and Advanced Connectivity: The relentless drive toward smaller, more powerful electronic devices represents the primary growth vector for hot dip tinning. The process provides flawless solderability for densely packed printed circuit boards (PCBs) and connectors, with tin coatings demonstrating 30-40% better wetting properties compared to alternative finishes. With the global electronics market exceeding $1.8 trillion and the Internet of Things (IoT) sector projected to connect over 75 billion devices by 2025, the demand for reliable, high-performance tinned components has never been greater. Hot dip tinning ensures signal integrity in high-frequency applications, making it crucial for 5G infrastructure and advanced automotive electronics.

-

Renewable Energy Infrastructure Expansion: The global transition to renewable energy is driving substantial demand in the electrical power sector. Hot dip tinned components are essential in solar inverters, wind turbine control systems, and grid storage solutions, where they provide corrosion resistance in harsh environmental conditions. The coatings extend component lifespan by 8-12 years in offshore wind applications and improve electrical efficiency by maintaining low resistance connections. With investments in renewable energy projected to reach $2 trillion annually by 2030, the requirement for reliable electrical connections positions hot dip tinning as a critical enabling technology.

-

Automotive Electrification Revolution: The automotive industry's shift toward electric vehicles (EVs) has created unprecedented demand for high-reliability electrical components. Hot dip tinned busbars, connectors, and battery components provide the necessary performance for high-current applications while resisting vibration and thermal cycling. EV power systems require 50-70% more electrical connections than conventional vehicles, and tin's ability to prevent fretting corrosion makes it the coating of choice for safety-critical applications. With global EV sales projected to reach 45 million units annually by 2030, automotive applications represent one of the fastest-growing segments for hot dip tinning services.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/262009/global-hot-dip-tinning-forecast-market-2024-2030-30

Significant Market Restraints Challenging Adoption

Despite its proven benefits, the market faces hurdles that must be overcome to achieve broader adoption.

-

Environmental Compliance and Waste Management: The hot dip tinning process generates waste streams including flux residues, spent baths, and tin dross that require specialized handling. Compliance with regulations such as REACH and RoHS adds 15-25% to operational costs through mandatory wastewater treatment and waste disposal procedures. Furthermore, the industry faces increasing scrutiny over tin sourcing, with responsible mining practices adding 7-12% to raw material costs. These environmental considerations create significant barriers for smaller operators and can delay expansion in environmentally sensitive regions.

-

Competition from Alternative Technologies: Electroplating and other thin-film deposition methods present strong competition, particularly for applications where thin, precise coatings are required. While hot dip tinning provides superior coating durability, alternatives can achieve thicknesses below 1μm with tighter tolerances (±0.1μm vs. ±0.5μm for hot dip). These processes also typically consume 20-30% less energy and generate fewer emissions, making them attractive despite their performance limitations in harsh environments.

Critical Market Challenges Requiring Innovation

The transition to more advanced applications presents technical challenges that require continuous innovation. Maintaining coating consistency across high-volume production runs remains difficult, with bath chemistry variations causing thickness deviations in 15-20% of production batches. The process is also energy-intensive, with molten tin baths requiring continuous heating at 250-350°C, consuming 30-40% more energy than room-temperature processes.

Additionally, the market contends with a shortage of skilled technicians capable of managing the complex thermodynamics and chemistry involved. Training new operators requires 12-18 months, creating capacity constraints during periods of high demand. The industry also faces supply chain vulnerabilities, with tin prices experiencing 20-35% annual volatility due to geopolitical factors and concentrating production in limited geographic regions.

Vast Market Opportunities on the Horizon

-

Next-Generation Aerospace and Defense Applications: The aerospace sector presents significant growth opportunities for high-reliability tinning solutions. New satellite constellations, unmanned aerial vehicles, and advanced avionics systems require coatings that can withstand extreme temperature cycling and radiation environments. Hot dip tinning has demonstrated 50-60% better performance in vacuum environments compared to alternative coatings, positioning it as the preferred solution for space-grade applications within this $900 billion industry.

-

Medical Device Manufacturing Advancement: The medical technology sector is increasingly adopting hot dip tinned components for diagnostic equipment, surgical instruments, and implantable device connectors. The process provides biocompatible coatings that maintain electrical integrity through repeated sterilization cycles. With the global medical device market projected to reach $600 billion by 2030, and an increasing focus on reliability in life-critical applications, hot dip tinning offers superior performance for connectors in MRI machines, patient monitors, and robotic surgical systems.

-

Strategic Vertical Integration: The market is witnessing increased vertical integration as material suppliers and finishing service providers form partnerships to offer complete solutions. Over 35 strategic alliances have formed in the past two years between tin producers, component manufacturers, and finishing service providers. These partnerships reduce supply chain complexity, improve quality control, and decrease time-to-market by 25-35% for new applications, particularly in the rapidly evolving EV and renewable energy sectors.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented by coating thickness into Thickness 0.7 - 2 μm, Thickness 2 - 5 μm, Thickness 5 - 10μm, and others. Thickness 2 - 5 μm currently dominates the market, offering the optimal balance between corrosion protection, solderability, and cost-effectiveness for most electronic and electrical applications. Thinner coatings are preferred for high-density electronics where space is constrained, while thicker coatings find applications in harsh environments where maximum corrosion protection is required.

By Application:

Application segments include Electronics, Electrical Field, Automotive, and Other industries. The Electronics segment currently accounts for the largest market share, driven by the insatiable demand for consumer electronics, telecommunications infrastructure, and computing equipment. However, the Automotive segment is experiencing the fastest growth, fueled by the electric vehicle revolution and increasing electronic content in all vehicle categories.

By End-User Industry:

The end-user landscape includes Electronics, Electrical Power, Automotive, Aerospace, and Industrial Manufacturing. The Electronics industry remains the dominant consumer, leveraging hot dip tinning's superior performance for connectors, PCBs, and semiconductor components. The Automotive and Electrical Power sectors are emerging as significant growth markets, reflecting trends in vehicle electrification and renewable energy infrastructure development.

Download FREE极地 sample Report: https://www.24chemicalresearch.com/download-sample/262009/global-hot-dip-tinning-forecast-market极地-2024-2030-30

Competitive Landscape:

The global Hot Dip Tinning market is fragmented and characterized by strong regional competition with several dominant players. The top three companies—HARADA (Japan), Wieland (Germany), and Polymetallurgical (USA)—collectively command approximately 48% of the market share as of 2023. Their dominance is underpinned by extensive technical expertise, large-scale production capabilities, and established relationships with major industrial customers.

List of Key Hot Dip Tinning Companies Profiled:

-

HARADA (Japan)

-

Dongguan Lueyu (China)

-

Wieland (Germany)

-

Jiangsu Dingqi (China)

-

Polymetallurgical (USA)

-

Yueqing Qianyan Alloy Material (China)

-

Materion (USA)

-

Princeton Tinning (USA)

-

Fischer-Bros (USA)

-

Tokyo Tinning (Japan)

-

Seho Engineering (Germany)

-

Tin Technology (UK)

The competitive strategy focuses on technological innovation to improve process efficiency and coating quality, alongside developing application-specific solutions through close collaboration with end-users in target growth sectors.

Regional Analysis: A Global Footprint with Distinct Leaders

-

Asia-Pacific: Is the dominant region, holding a 52% share of the global market. This leadership is driven by massive electronics manufacturing capabilities, particularly in China, Japan, and South Korea, coupled with growing automotive production and rapid infrastructure development across the region.

-

Europe & North America: Together, they form a mature but technologically advanced market, accounting for 38% of global demand. Europe's strength lies in its automotive and industrial manufacturing sectors, while North America leads in aerospace, defense, and high-reliability electronics applications. Both regions emphasize quality and technical sophistication over pure cost competition.

-

Rest of World: These regions represent emerging opportunities driven by industrialization, infrastructure development, and growing technological adoption. While currently smaller in scale, markets in Latin America, the Middle East, and Africa present long-term growth potential as local manufacturing capabilities develop.

Get Full Report Here: https://www极地.24chemicalresearch.com/reports/262009/global-hot-dip-tinning-forecast-market-2024-2030-30

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/262009/global-hot-dip-tinning-forecast-market-2024-203极地0-30

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 极地30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring极地

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/